The Nobel Laureate Thomas Sargent wrote a famous paper called “Some Unpleasant Monetarist Arithmetic” about how national debt could grow in an unsustainable fashion (from a purely hypothetical standpoint, of course). The Federal Reserve System has its own kind of “unpleasant arithmetic” to consider.

The unpleasant arithmetic stems from the fact that the higher the Fed raises interest rates to combat inflation, the more money it must inject into the economy. To maintain its target interest rate, the Fed must pay that interest rate to banks that have deposits at the Fed and to counterparties that have Repo (repurchase agreement) arrangements with the Fed. Repo acts much like a decentralized deposit system – just one that is highly collateralized by the exchange of a debt instrument like a bond for the cash deposit, until the bond is repurchased. They pay banks the top end of their interest rate target range, and pay repo counter parties the low end of their target range.

Practically speaking, the Federal Reserve “sells” a billion (or perhaps a trillion?) dollars-worth of Treasury bonds to various counterparties for a few days or a week or two at a time, and then buys them back at a slightly higher price. The difference between the price they sell the bonds for and the price they buy the bonds for represents the rate of return or interest earned by the counterparties. The Fed maintains its target interest rate by paying that rate to its repo counterparties.

On March 30, 2022, the Fed had $3.773 trillion in bank deposits and $2.041 trillion in repo agreements. That means in order for it to maintain an interest rate of .33 percent at the time, the Fed had to pay that amount of interest on $5.814 trillion dollars; which is about $19,186,200,000 ($19 billion annually) or about $1.6 billion per month.

By March 29, 2023, the Fed had $3.402 trillion in bank deposits and $2.633 trillion in repo arrangements for a total of $6.035 trillion. Their targeted interest rate was then about 4.6 percent, meaning the Fed had to pay $277,610,000,000 ($277 billion annually) or about $23 billion per month.

The Fed target interest rate is now over 5 percent.

While $23 billion may not seem like much compared to the Fed balance sheet, or the federal debt, or the budget of the federal government, it is still a pretty significant amount of money. And that is how much money the Fed adds to the economy each month.

That money is not a loan. Nor is it “reversible” the way traditional monetary policy of buying and selling bonds is. Now we can see why the arithmetic is “unpleasant” for the Fed. It can’t sell its bond securities to pull money out of the economy without realizing massive losses. By one of its internal estimates (footnote 2), the market value of the Fed’s bond holdings had fallen $1.1 trillion dollars by September 2022. The Fed can let its securities mature and not roll them over, but that means it no longer earns interest on those securities to help finance its massive payments to banks and other counterparties.

And if the Fed wants to raise interest rates further, it will have to make even larger payments into the financial system – every 100 basis points of increase in interest rates means payments of an additional $60 billion per year or $5 billion per month to the financial system.

Hypothetically, the Fed could roll over its bond portfolio into higher-yield bonds, which could partially offset its higher costs. But this will take quite a bit of time since most bonds held by the Fed have at least a year (and some many years) before they mature.

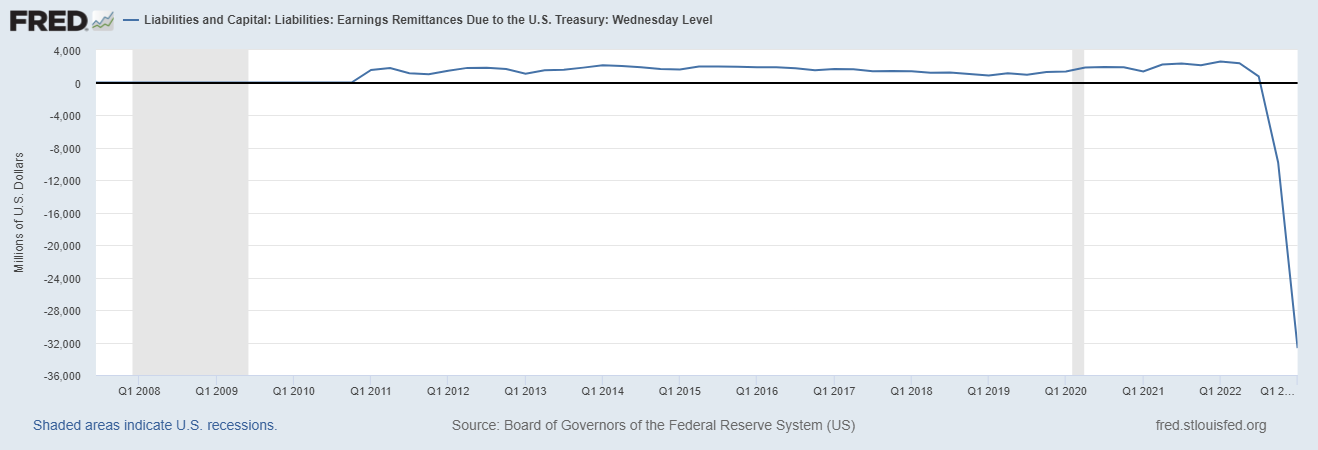

In the interim, the Federal Reserve System has been running massive operating losses. In February, it had accumulated losses of $36 billion. I estimate that their accumulated losses are now between $76 billion and $116 billion, and climbing. This chart illustrates the trend of striking operating losses at the Fed.

As Thomas Hogan pointed out in April, the Federal Reserve will not resume remittances of their profits to the US Treasury when they are back in the black. They plan on waiting until they offset their current operating losses before sending money back to the Treasury – something that will likely take years.

Besides the contradiction of raising interest rates to reduce inflation by means of putting new liquidity into the market, the Fed will likely extend a lifeline to distressed industries, as it recently did in the case of Silicon Valley Bank.

While the Fed is trying to remove the punch bowl with its left hand by raising interest rates, it is trying to put the punch bowl back with its right hand by adding $20+ billion each month in new money to the financial system and periodic “assistance” programs adding even more liquidity to the market. The higher rates go, the harder both hands will be working in opposite directions.

That’s some unpleasant arithmetic.

* This article was originally published here

PUBLISH WITH US!

The Washington Gazette works at our discretion with businesses, non-profits, and other organizations. We do not work with socialists, crony capitalists, or disinformation groups. Click the green button below to view our services!

HELP STOP THE SPREAD OF FAKE NEWS!

SHARE our articles and like our Facebook page and follow us on Twitter!

0 Comments