Total housing starts fell to a 1.439 million annual rate in September from a 1.566 million pace in August, an 8.1 percent drop. From a year ago, total starts are down 7.7 percent. However, total housing permits rose in September, posting a 1.4 percent gain to 1.564 million versus 1.542 million in August. Total permits are still down 3.2 percent from the September 2021 level.

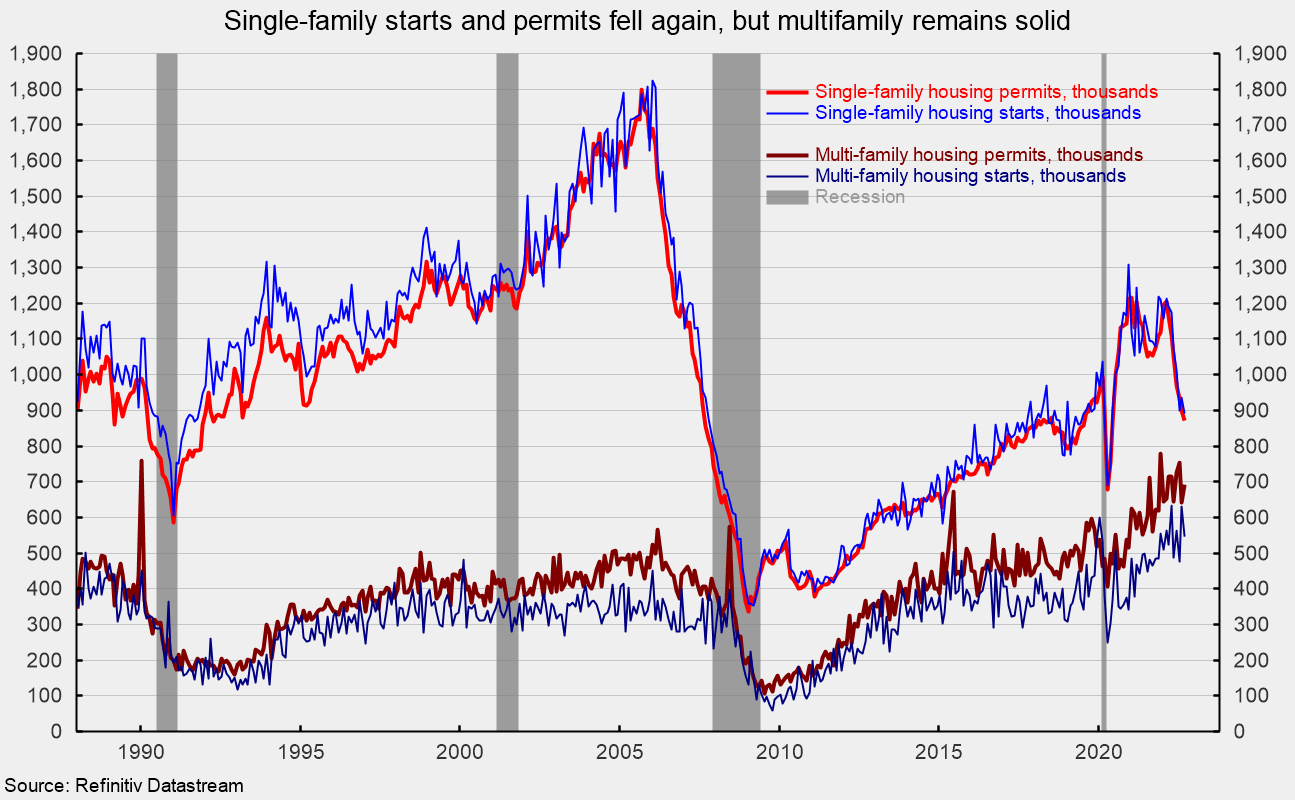

Starts in the dominant single-family segment posted a rate of 892,000 in September versus 936,000 in August, a drop of 4.7 percent. That is the third consecutive month under one million and the slowest pace since May 2020. Starts are down 18.5 percent from a year ago (see first chart). Single-family permits fell 3.1 percent to 872,000 versus 900,000 in August, the fourth consecutive month under one million and the slowest pace since June 2020 (see first chart).

Starts of multifamily structures with five or more units decreased 13.1 percent to 530,000 but are up 16.5 percent over the past year, while starts for the two- to four-family-unit segment fell 15.0 percent to a 17,000-unit pace versus 20,000 in August. Total multifamily starts were off 13.2 percent to 547,000 in September, but still showing a gain of 17.6 percent from a year ago (see first chart). However, multifamily permits for the 5-or-more group rose 8.2 percent to 644,000, while permits for the two-to-four-unit category increased 2.1 percent to 48,000. Total multifamily permits were 692,000, up 7.8 percent for the month and 23.4 percent from a year ago (see first chart).

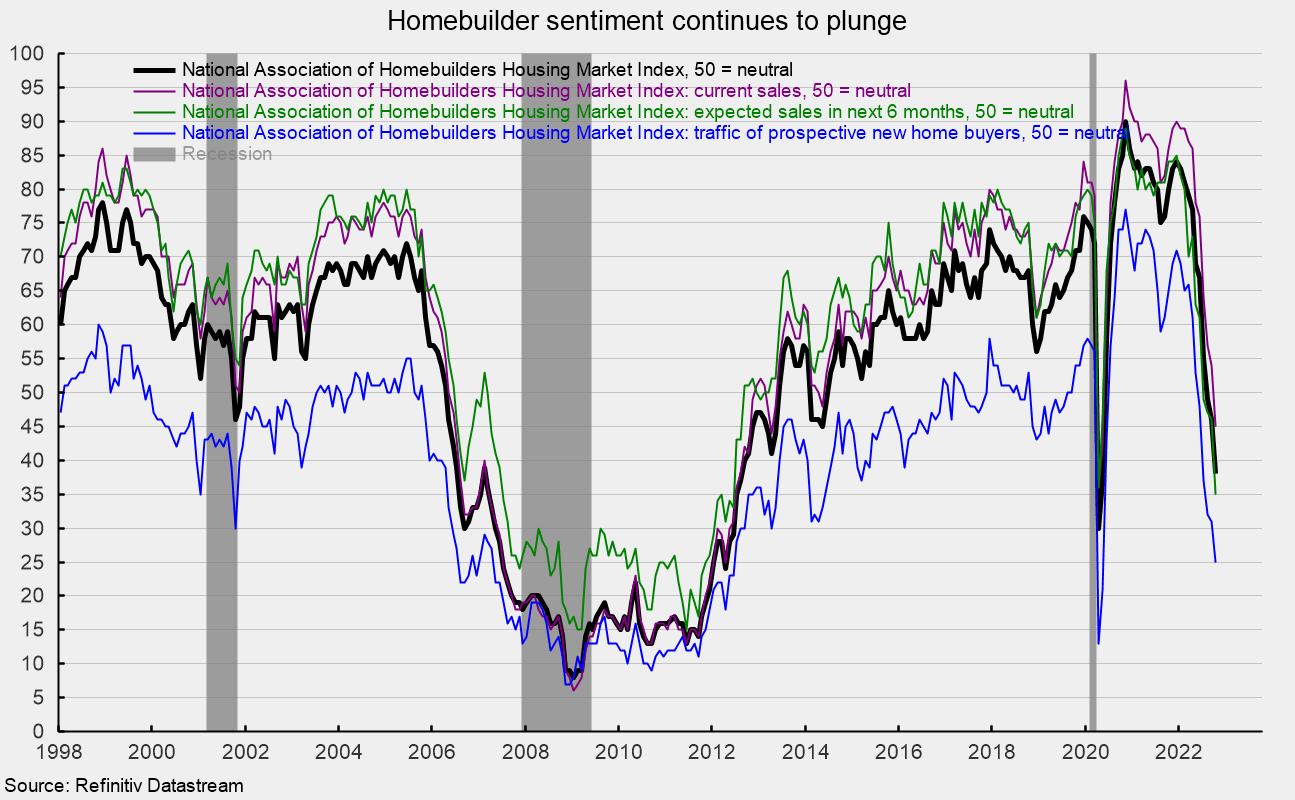

Meanwhile, the National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, fell again in October, coming in at 38 versus 46 in September. That is the tenth consecutive drop and the third consecutive month below the neutral 50 threshold. The index is down sharply from recent highs of 84 in December 2021 and 90 in November 2020 (see second chart).

All three components of the Housing Market Index fell again in October. The expected single-family sales index dropped to 35 from 46 in the prior month, the current single-family sales index was down to 45 from 54 in September, and the traffic of prospective buyers index sank again, hitting 25 from 31 in the prior month (see second chart).

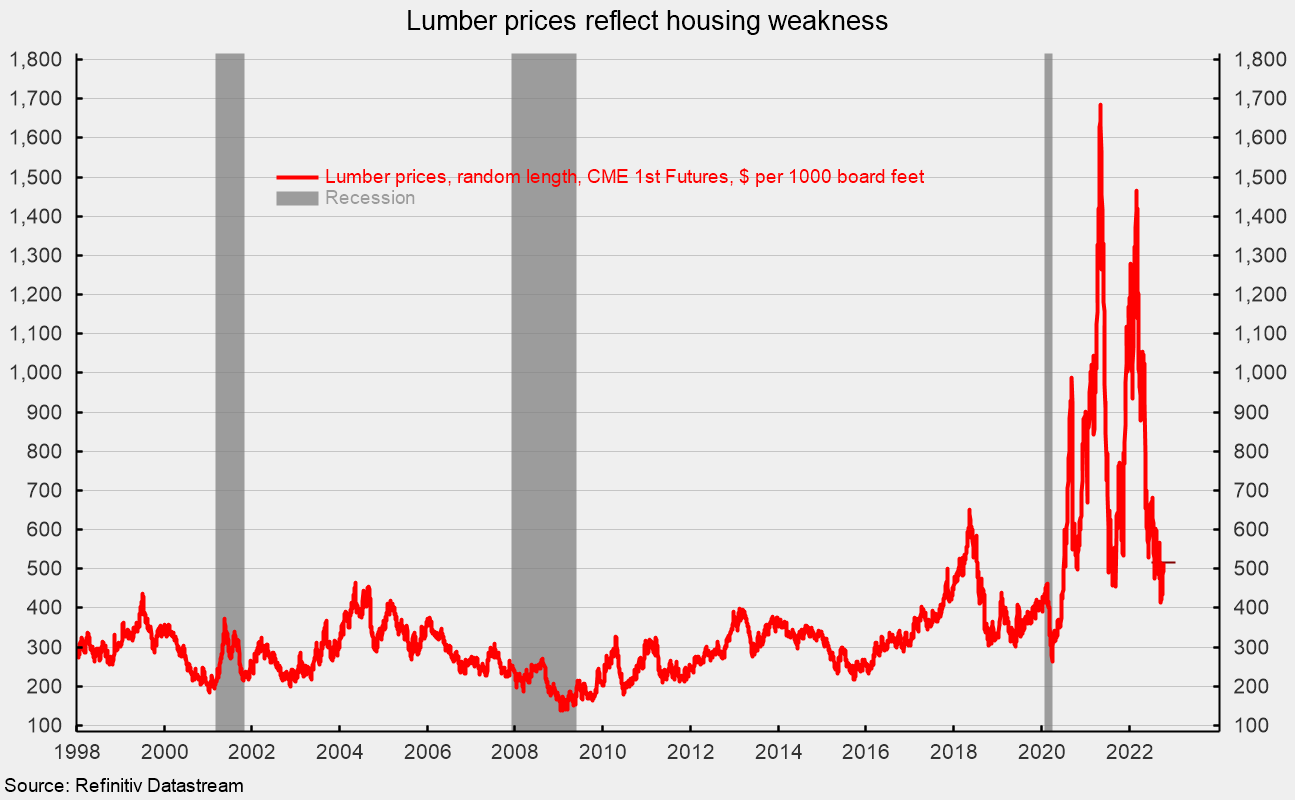

Input costs and supply delivery problems are still concerns for builders though lumber prices have declined sharply from recent highs. Lumber recently traded around $517 per 1,000 board feet in mid-October, down from peaks around $1,700 in May 2021 and $1,500 in early March 2022 (see third chart).

Mortgage rates continue to surge, with the rate on a 30-year fixed rate mortgage coming in at 6.92 percent in mid-October versus 5.13 percent in late August. Rates are up more than 400 basis points, more than double the lows in early 2021 (see fourth chart).

While the implementation of permanent remote working arrangements for some employees may have been providing continued support for housing demand, record-high home prices combined with the surge in mortgage rates and cautious consumer attitudes are working to weaken demand. Pressure on housing demand combined with elevated input costs is sending homebuilder sentiment plunging. The outlook for housing is unfavorable.

* This article was originally published here

PUBLISH WITH US!

The Washington Gazette works at our discretion with businesses, non-profits, and other organizations. We do not work with socialists, crony capitalists, or disinformation groups. Click the green button below to view our services!

HELP STOP THE SPREAD OF FAKE NEWS!

SHARE our articles and like our Facebook page and follow us on Twitter!

0 Comments