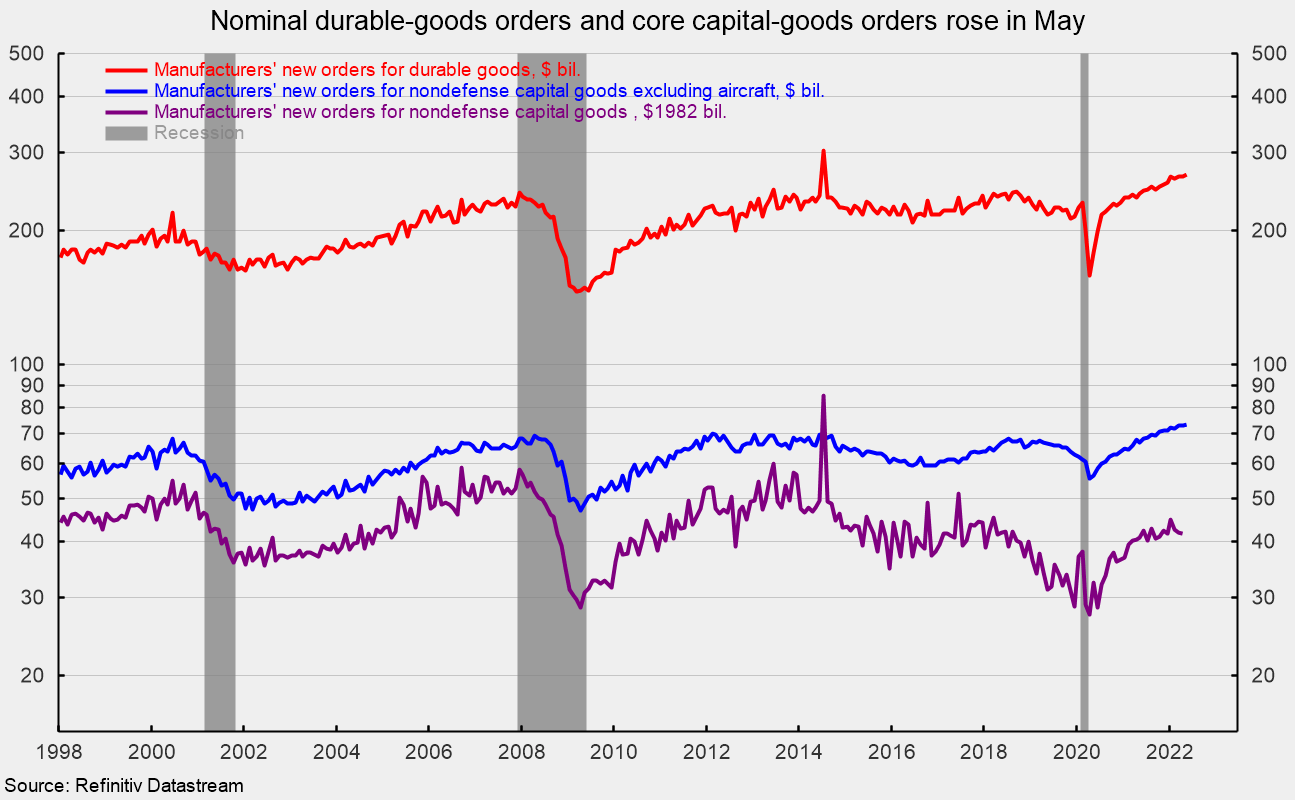

New orders for durable goods increased 0.7 percent in May, following a 0.4 percent gain in April, the 11th increase in the last 13 months. Total durable-goods orders are up 10.0 percent from a year ago. The May gain puts the level of total durable-goods orders at $267.2 billion, the second highest on record (see first chart).

New orders for nondefense capital goods excluding aircraft, or core capital goods, a proxy for business equipment investment, rose 0.5 percent in May after increasing 0.3 percent in April. Orders are up 6.4 percent from a year ago, with the level at $73.4 billion, a new record high (see first chart).

However, rapid price increases have an impact on capital goods orders. In real terms, after adjusting for inflation, real new orders for nondefense capital goods – one of AIERs leading indicators – were $41.7 billion in April, measured in 1982 dollars, a solid level by historical comparison but well shy of the record high (see first chart). Furthermore, producer prices for capital equipment rose 0.7 percent in May, suggesting that in real terms, new orders for nondefense capital goods may have declined in May.

Nearly every major category (six of seven) in the durable-goods report showed a gain in May. Among the major individual categories, primary metals led with a 3.1 percent increase, followed by machinery orders and transportation equipment orders with increases of 1.1 percent and 0.8 percent, respectively. Computers and electronic products gained 0.5 percent while all other durables added 0.2 percent. Within the transportation equipment category, motor vehicles and parts were up 0.5 percent, but nondefense aircraft fell 1.1 percent, and defense aircraft gained 8.1 percent. Electrical equipment and appliances fell 0.9 percent (see second chart). From a year ago, every major category shows a solid gain.

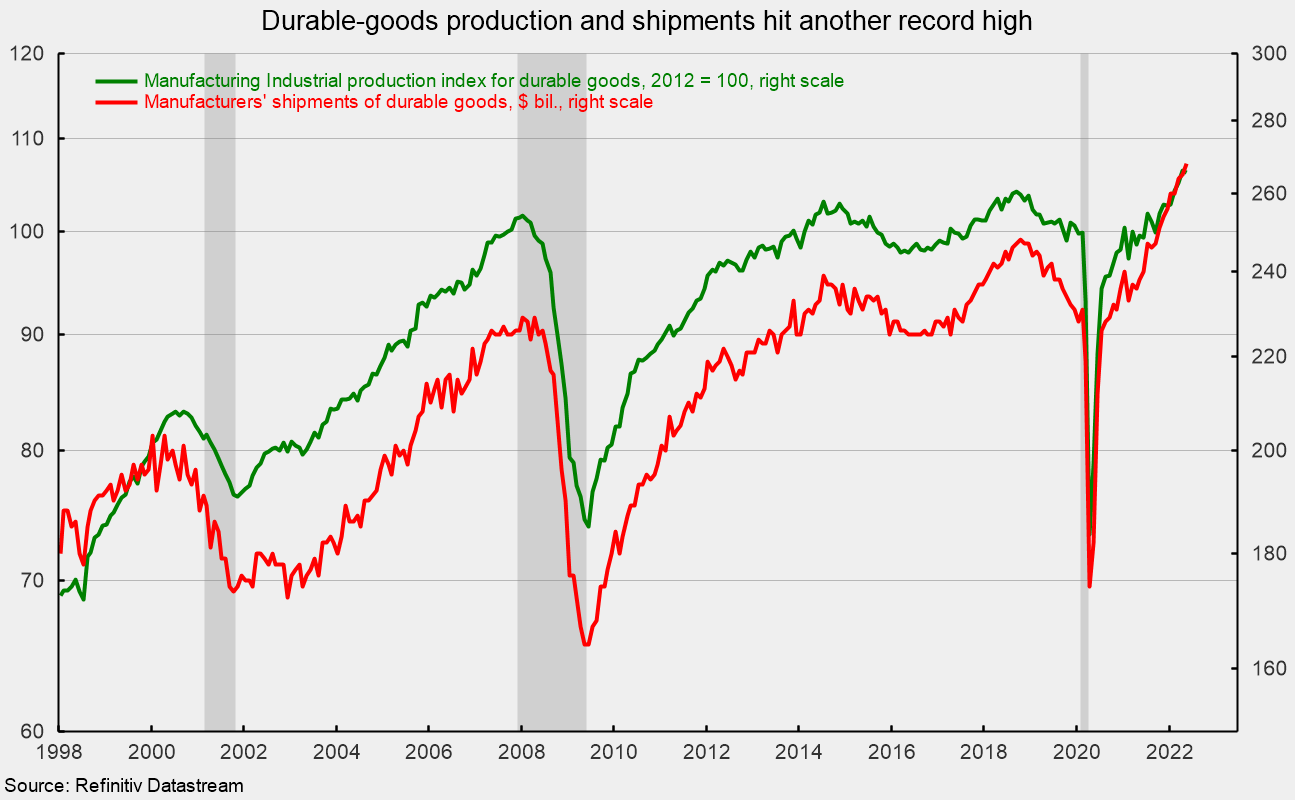

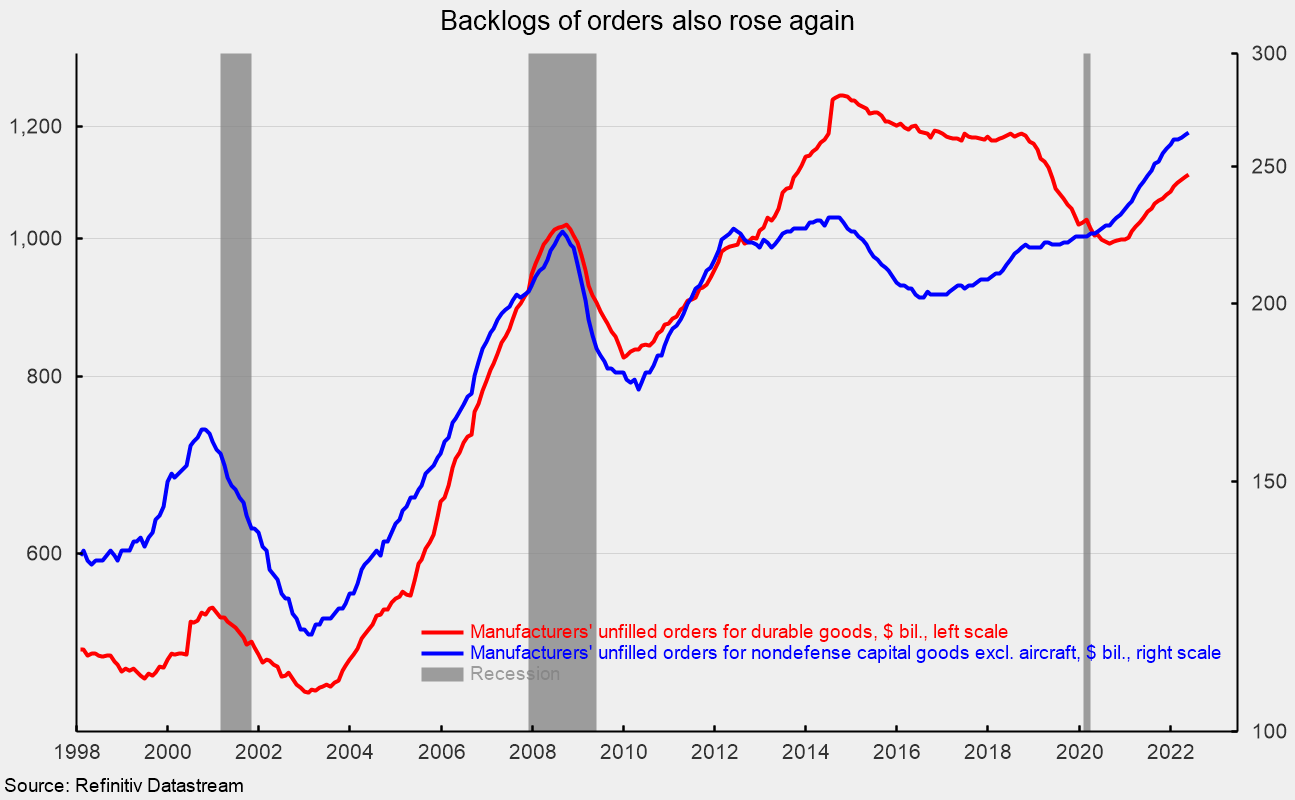

Despite the difficulties in finding and retaining labor, materials shortages, and logistical problems, durable-goods output has been increasing. Output, as measured by industrial production for durable goods from the Federal Reserve and the value of manufacturers’ shipments of durable goods, are well above the peaks in 2018 before the lockdown recession of 2020 (see third chart). Yet, backlogs of orders continue to rise, with backlogs of core capital goods at a record high (see fourth chart).

Durable-goods orders continue to be strong, particularly the core-capital goods components, though some of the gain in nominal-dollar orders is due to price increases. Demand remains robust for the manufacturing sector, and the tight labor market creates incentives to substitute capital for labor.

However, the outlook remains uncertain. Sustained upward pressure on prices continues as demand outpaces supply. Labor and materials shortages continue to hamper production while the fallout from the Russian invasion of Ukraine and periodic lockdowns in China continue to disrupt global supply chains. Furthermore, the Federal Reserve has begun an interest rate tightening cycle, boosting the probability of a policy mistake. Caution is warranted.

* This article was originally published here

PUBLISH WITH US!

The Washington Gazette works at our discretion with businesses, non-profits, and other organizations. We do not work with socialists, crony capitalists, or disinformation groups. Click the green button below to view our services!

HELP STOP THE SPREAD OF FAKE NEWS!

SHARE our articles and like our Facebook page and follow us on Twitter!

0 Comments