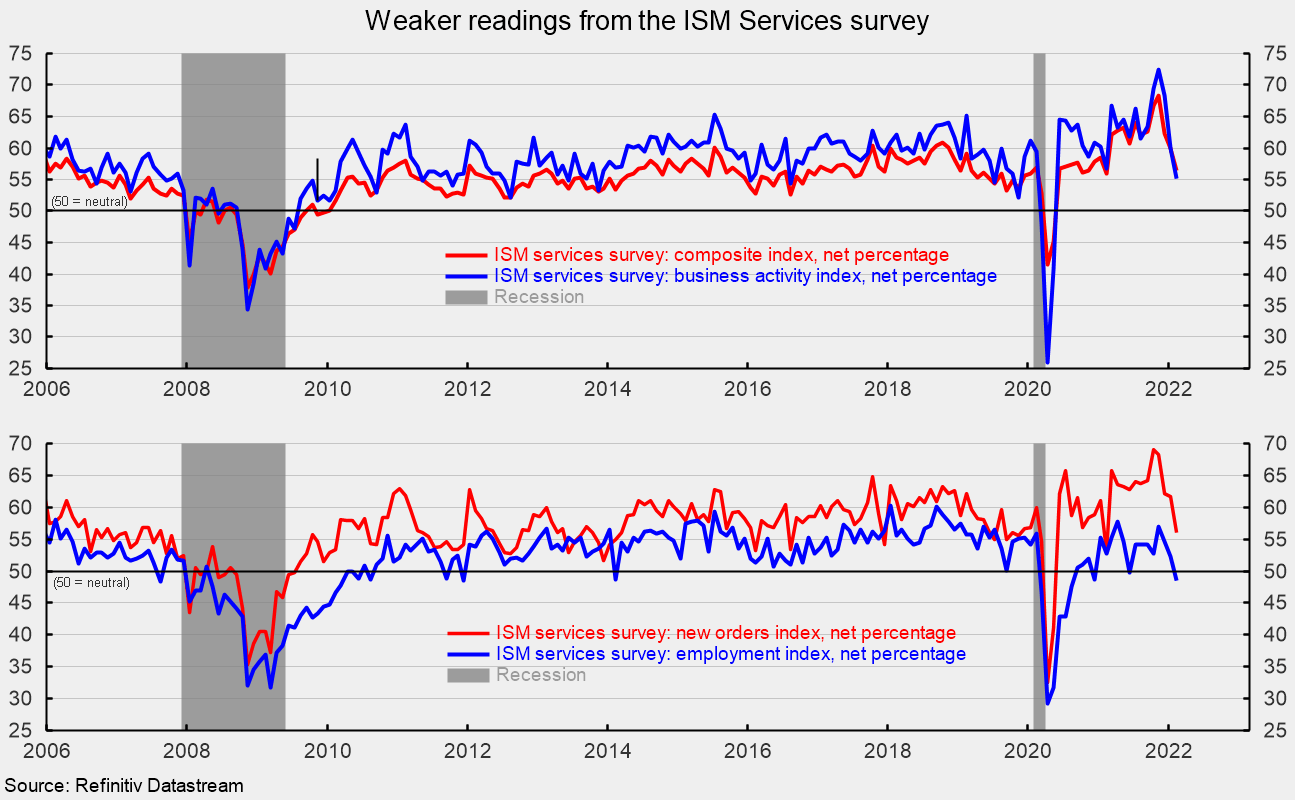

The Institute for Supply Management’s composite services index fell to 56.5 percent in February, losing 3.4 points from 59.9 percent in the prior month. The index remains above neutral and suggests the 21st consecutive month of expansion for the services sector and the broader economy but is now at its lowest level since February 2021 (see top of first chart). The declines over the last three months suggest that growth has likely slowed with respondents to the survey blaming labor shortages and turnover, materials shortages, logistical issues, and price pressures.

Among the key components of the services index, the business activity index fell 4.8 points to 55.1 (see top of first chart). That is the 21st month above 50 but also the lowest reading since a 40.9 result since May 2020 in the aftermath of government shutdowns that caused the worst recession in American history.

The services new-orders index fell to 56.1 percent from 61.7 percent in January, a drop of 5.6 percentage points (see bottom of first chart). The new orders index has been above 50 percent for 21 months but is now at the lowest level since February 2021. For the latest month, 11 industries reported expansion in new orders while three reported drops.

The nonmanufacturing new-export-orders index, a separate index that measures only orders for export, rebounded in February, coming in at 53.0 versus 45.9 percent in January. Seven industries reported growth in export orders against two reporting declines.

Backlogs of orders in the services sector likely grew again in February as the index increased to 64.2 percent from 57.4 percent. February was the 14th month in a row with rising backlogs. Thirteen industries reported higher backlogs in February while three reported a decrease. The services employment index dropped below the neutral 50 percent level, coming in at 48.5 percent in February, down from 52.3 percent in January and a recent high of 57.0 percent in November (see bottom of first chart). Seven industries reported growth in employment while eight reported a reduction.

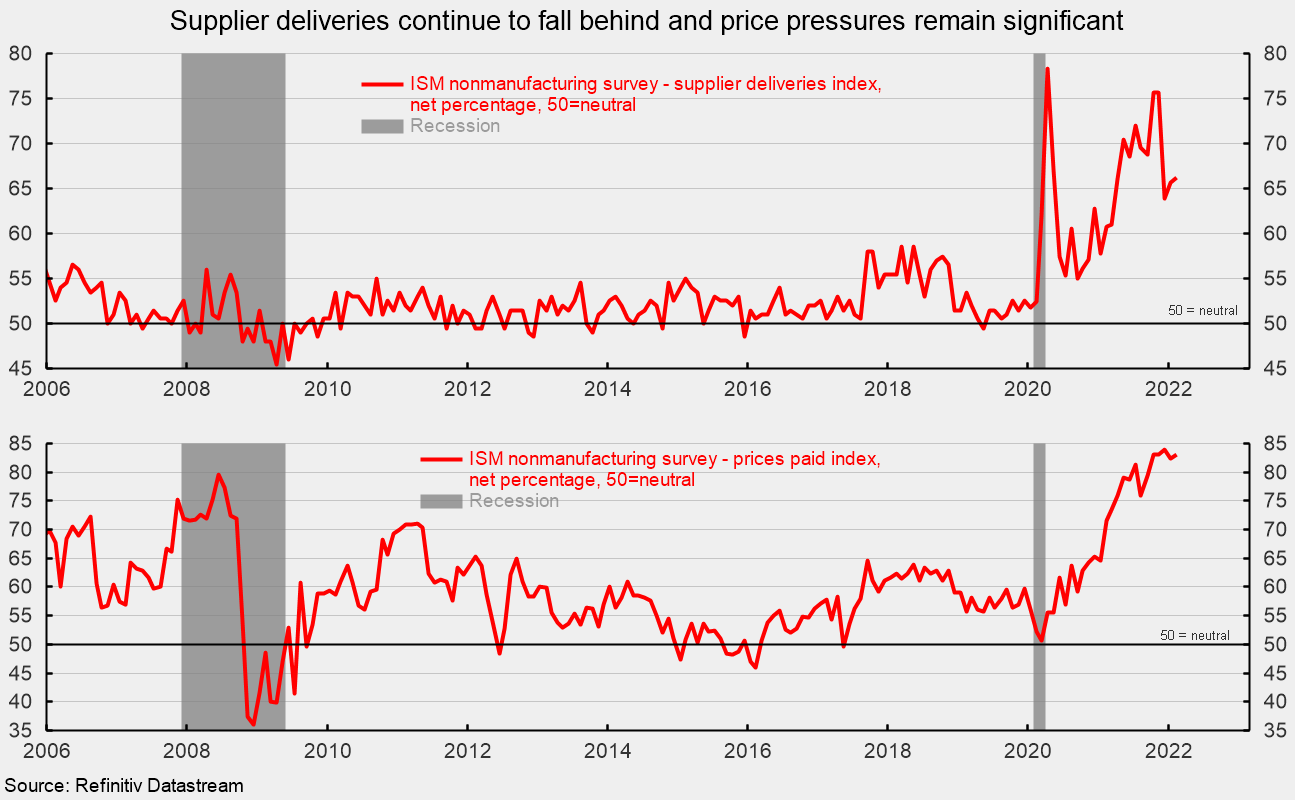

Supplier deliveries, a measure of delivery times for suppliers to nonmanufacturers, came in at 66.2 percent, up from 65.7 percent in the prior month (see top of second chart). It suggests suppliers are falling further behind in delivering supplies to services business and the slippage accelerated slightly from the prior month. Sixteen industries reported slower deliveries in February while none reported faster deliveries.

The nonmanufacturing prices paid index rose to 83.1 percent, up from 82.3 percent in January, and just below the all-time high in December 2021 (see bottom of second chart). Eighteen industries reported paying higher prices for inputs in February while none reported lower prices.

The February report from the Institute of Supply Management suggests that the services sector and the broader economy expanded for the 21st consecutive month in February. Respondents to the survey continue to highlight strong demand but also continued price pressures, materials shortages, logistics, and transportation issues, and challenges hiring and retaining workers. As the latest wave of Covid crests, some improvement in production is expected, but the overall shortage of labor is likely to be a lingering problem. Furthermore, geopolitical turmoil as a result of the Russian invasion of Ukraine has had a dramatic impact on capital and commodity markets, launching a new wave of potential disruptions to the global economy and businesses. The outlook has become highly uncertain.

* This article was originally published here

PUBLISH WITH US!

The Washington Gazette works at our discretion with businesses, non-profits, and other organizations. We do not work with socialists, crony capitalists, or disinformation groups. Click the green button below to view our services!

HELP STOP THE SPREAD OF FAKE NEWS!

SHARE our articles and like our Facebook page and follow us on Twitter!

0 Comments